One of my friends is eager to start his own business. my friend has saved 10,000 £, but he knows that he needs at least 30,000£ to start a business. In order to start a business, employees must be paid, and factories must be operated, so they must seek funds to use in the short term. Additional funds are also needed to develop new products to suit the tastes of consumers who have changed in the long run. In this way, companies must raise funds for various purposes while running their businesses. I would like to learn about various ways companies raise funds.

The company’s funds are divided into internal and external finance according to the financing method. Among the funds a company needs, internal finance is covered by funds accumulated inside the company, that is, internal funds, through corporate savings such as internal reserves and depreciation reserves. However, since it is difficult to raise funds for companies with internal funds, it goes through the process of borrowing and raising funds necessary for investment projects from outside, which is called external finance. External finance includes indirect finance and direct finance. The former is borrowing from banks, and the latter is to raise funds by issuing bonds or bills in the stock market.

The way companies raise funds from outside can be largely divided into borrowing and receiving investment. The first way to borrow funds is for a company to pay interest regularly according to a set promise and repay the principal at maturity, which is called “other capital,” meaning other people’s money. The method of borrowing funds can be divided into indirect finance that borrows funds through banks and direct finance that issues corporate bonds (bonds) to investors without going through banks. Indirect financing is similar to individuals taking out loans from banks, while direct financing, which issues corporate bonds, is a unique financing method for companies. In the case of borrowing and using funds, companies have the advantage of being able to operate their business without external interference, while paying interest and principal on a set date regardless of profits and losses.

Receiving investment, the second method, is expressed as receiving ‘investment’, and the funds invested are called ‘ownership capital’. Investors are also involved in management because they become the owner of the company by the percentage of their investment in the total stake. Investors are interested in whether the investment amount is being used properly for corporate management because they will receive as much of the company’s profits as they have invested. The most representative way a company receives external investment is to issue stocks, which are certificates representing ownership of the company. If a company raises funds by receiving investment from outside, the company is stable in managing funds because it is not obliged to pay back the principal and interest, but as various people become the owners of the company, investors may be excessively involved in corporate management.

Since each company has different purpose of financing, size and timing of necessary funds, financial status, and management philosophy, companies decide the most appropriate financing method by considering various factors when financing. Individuals who supply funds to companies also need to pay attention to the company’s financing methods and refer to them when investing.

A stakeholder is a person who has an interest in a company. Here, understanding refers to literal interests and damages, not interests that distinguish and interpret reason. In other words, the actions of some members may benefit from financial and non-monetary desirable action results for other members or groups, or may cause damage as undesirable action results. Such interests and damages to members or groups are collectively referred to as understanding.

The stakeholder group is a group of people with these interests. It includes not only shareholders but also consumers, suppliers, employees, local communities, media, environment, and civic groups.

The classification of stakeholder groups can be divided into five categories as follows.

- Shareholders: In fact, as the owner of the company, they are members of the general shareholders’ meeting, the best decision-making body of the company.

- Financial companies: As a group that has a great influence on the business environment and management decision-making, the capital raising problem of a company is enormous, so it relies on the support of financial companies in the capital market rather than shareholders. For companies, raising capital is essential and financial capabilities always occupy a large proportion of corporate strategic decisions, so the influence of financial institutions among corporate stakeholders is terrifying.

- Supplier: Supplier is a company that supplies raw materials, raw materials, parts, and semi-finished products to a company, including subcontractors. In the long run, it is important to maintain a good relationship with each other so that companies can survive and grow in balance in mutual stakeholders by providing financial and technical support to suppliers.

- Consumer: As a stakeholder in the corporate environment, the factor that has the greatest influence is consumer. Today, corporate management strategies must be customer-oriented. Therefore, it is consistent with the corporate objectives of customer creation, market creation, and demand creation.

- Employees: The influence of trade unions and employees is gradually increasing. As companies grow, employees grow together, so if the demands or opinions of labor unions and employees created as a group of stakeholders are sufficiently reflected in corporate activities, companies can act as interdependent and democratic organizations.

A company’s stakeholder refers to an individual or group with an interest in the company, and in addition to shareholders and bondholders, workers, consumers, and subcontractors are included as corporate stakeholders, so their relationship can be considered important.

- Budget composition

- General budget rules and revenue expenditure.

- General term for budget, continuous expenses, carryover expenses and the burden of national treasury debt.

- General budget rules

- The general budget rules are called the general budget rules, and the general budget rules stipulate the limit of government bonds or borrowings, issuance of financial securities, the highest amount of temporary borrowings, and other necessary matters.

- The maximum amount of issuance of financial securities and borrowing of lump sum loans must be resolved by the National Assembly every accounting year for each accounting year.

- Three bites.

- It refers to all cash income that is the expenditure resource of the State or local government in a certain fiscal year.

- The main national tax revenue is tax revenue, including income from public bonds, sales of state-owned property, income from government enterprises, and commission income.

- However, even if stored in the national treasury, it does not include deposits, postal deposits, deposits, etc. of bids and contracts that cannot cover the financial resources of expenditures.

- Expenditure.

- Any expenditure by the State or local government to fulfill its purpose in a fiscal year includes payment of public officials’ salaries, purchase of goods and services, payment of interest and subsidies, acquisition of fixed assets, and expenditure for repayment of public bonds.

- Expenditures, unlike revenues, can only be spent within budget.

- Continuous rain

- Construction or manufacturing and R&D projects that require years of completion may be spent over several years within the scope of obtaining a resolution by the National Assembly in advance by determining the total amount and annual amount of expenses.

- In executing the established continuous expenses, the amount of expenditure not spent in the relevant year is carried forward by the relevant continuous expenditure business year, but there is a limit that it can be spent only within five years from the relevant year.

- However, if deemed necessary, the period may be extended again through a resolution of the National Assembly (exceptions to the principle of independence in the accounting year).

- Explicit carryover fee

- A system carried forward to the following year through a resolution of the National Assembly in advance, clarifying the nature of the expenditure budget or the purpose of not being able to finish spending within the year due to reasons incurred after budget establishment.

- Here, the nature of expenses is that there is a concern that the project subject to use of the expenses may not be completed within one fiscal year due to special reasons, and the expenditure of expenses cannot be completed within the year.

- The scope of carry-over shall be limited to the resolution, and once specified, expenses carried forward may act as the cause of expenditure in the following year, and accidents may be carried forward again for the carried-over expenses.

- A system carried forward to the following year through a resolution of the National Assembly in advance, clarifying the nature of the expenditure budget or the purpose of not being able to finish spending within the year due to reasons incurred after budget establishment.

- Temporary deposit

- It refers to borrowing and using funds from financial institutions to compensate for the temporary lack of funds in the world and repaying them as income within the current year, which is different from loans or government bonds in that lump sum loans cannot be a resource for expenditures.

- The expenditure budget should be spent as planned, regardless of actual income, but even if the balance is balanced throughout the fiscal year, expenditure may temporarily lead to a shortage of funds exceeding revenue.

- Since lump sum borrowings postpone the burden to a later date even within the same year, it should be noted that the actual income until the end of the year is accurately reviewed and predicted so that repayment is not impossible within the year.

- For a lump sum loan, the limit amount that can be temporarily borrowed every accounting year shall be determined by accounting and a resolution of the Council shall be obtained.

- The term “limit amount” means that the current amount cannot exceed it at any time, not the sum within the year, and that it can be carried out simultaneously with the resolution of the budget by stipulating it in the general budget rules of the parliament.

- It refers to borrowing and using funds from financial institutions to compensate for the temporary lack of funds in the world and repaying them as income within the current year, which is different from loans or government bonds in that lump sum loans cannot be a resource for expenditures.

As a result of analyzing the types of business budgets that Neil Down may have prepared for this business organization, since the industry is a toy store, we would like to recommend ways for new partners to make informed decisions on investment by analyzing operating budgets (sales, production, direct materials, direct labor, direct labor, overhead, general and management costs).

The method of determining the unit price of inventory assets is to determine the volume flow and cost flow (assuming the order in which inventory assets are sold if the unit price of inventory continues to fluctuate depending on the time of inventory acquisition), and can be largely divided into individual laws, first-in-first-out and second-in-first-out methods.

① Individual law

This is a method of separately recording the price purchased for each inventory and recording the purchase price of the inventory as the cost of sales when the inventory is sold. Individual laws are the most ideal way to match the flow of cost and real life, but in reality, if there are many types of inventory assets and transactions occur frequently, it is inconvenient to use in practice and expensive. For example, when cost identification is possible for each product, such as ordering and producing special machines, the cost can be determined using individual methods. However, it is not an appropriate way to apply this method to a large amount of homogeneous products that can be exchanged.

Advantages: The actual flow of supplies and the flow of costs can be accurately calculated.

Disadvantages: It is difficult to apply in reality because it takes a lot of time and money when there are many items or quantity of inventory.

② First-in-first-out method (FIFO)

First-in, first-out (FIFO) means that the oldest inventory items are recorded as sold first, but does not necessarily mean that the oldest items are tracked and then sold. In other words, the cost related to the inventory purchased first is the cost spent first. In addition to the first-in-first-out election law, the cost of inventory reported on the balance sheet represents the cost of inventory purchased most recently.

③ LIFO

The incoming and outgoing method is a method of determining the final inventory on the assumption that inventory items are sold or used in reverse order of purchase regardless of the actual flow of volume. It should be noted that unlike the first-in-first-out method, the final inventory and sales costs are calculated differently depending on which of the inventory recording methods are used!

Advantages: Response to current costs and current profits is the most appropriate way, which can be applied well to the principle of profit, that is, cost response, and corporate tax deferral effects can be seen in the case of inflation.

Disadvantages: Net profit for the term is indicated as the smallest, may not match the general volume flow, and final inventory is marked at past prices, which can distort financial analysis significantly.

Many founders think about whether to do corporate or private business when they first start a business. Corporate business operators are advantageous when comparing corporate tax of corporate businesses and comprehensive income tax of individual businesses simply with tax rates.

However, a corporation should not be judged to be advantageous just because the tax rate is nominally low. Income tax is levied again when an individual withdraws corporate property as a salary, bonus, or dividend, and if the corporation withdraws funds arbitrarily to avoid it, it can be embezzled under criminal law and treated as a (recognized) bonus, resulting in additional tax burden.

In the case of agonizing over private businesses and corporations, the composition of people and materials will be no different, whether it is a private business or a corporate business, because they usually plan to establish a company as a small investor.

If a corporation is established, it is mainly commissioned by a judicial scrivener and established in the form of a limited company or corporation. It is not that difficult to establish a corporation because it requires capital to establish a corporation, but now it is possible to establish a corporation without restrictions on the minimum capital.

It is the same for private and corporate businesses to register with the tax office and start the business. However, if you do business as a corporation, your business rights and obligations are greatly different from those of individual businesses. In the case of an individual business entity, it bears unlimited liability and rights for the business, but in the case of a business as a corporation or a limited company, it is only liable and rights as much as the capital invested as a shareholder (or employee). In other words, even if the corporate business is ruined, there is no obligation of an individual shareholder or CEO to repay the corporate debt except in the case of a joint guarantee.

However, with an exception to taxes, secondary tax obligations are imposed on shareholders who dominate the corporation (limited to equity holders exceeding 50%) to collect arrears taxes.

A corporation may be better in terms of such limited liability of investors. However, the corporation itself is an independent legal entity and is not the same as the CEO and shareholders. Therefore, the property of a corporation must be managed separately from the individual’s property.

It is often easy to think that if you make money through a corporation, you can arbitrarily withdraw the corporation’s money as a CEO or a single shareholder, but those who think so should not do corporate business. If the representative withdraws corporate funds arbitrarily, it is deemed that at least provisional payments (loans) or that the corporation has given bonuses to the representative, and taxes are imposed.

In addition, if the CEO withdraws the company’s money without paying the amount to be paid to the counterparty, he or she may be punished for embezzlement of public funds. On the other hand, private businesses can take and use all profits obtained through private businesses without any legal restrictions.

As mentioned earlier, if individual and corporate businesses make the same profits, corporations are advantageous in terms of immediate tax burden. However, CEO or shareholders cannot take the remaining profits recklessly after paying corporate taxes, and if they take them as salaries, bonuses or dividends, they will have to pay 6-42% of taxes as comprehensive income taxes again. Therefore, in a way, it can be a ginseng audit in terms of tax to do a corporate business.

At first, the corporate tax rate looks good because it is low, but later, it has to pay more taxes than private businesses. After all, it should not be considered based on taxes such as ‘corporate business or private business’. Decisions should be made by examining various factors such as business characteristics and fund management. However, a corporation will be advantageous for those who use shareholders’ limited responsibilities while doing large-scale projects or have no reason to accumulate considerable wealth in a corporation and withdraw it personally.

Mass discounting individual products means making a profit by selling a lot instead of making a small profit on the product. Since people prefer cheap products, one product itself does not have much profit, but they are trying to make a profit by selling them in large quantities. I think you can understand that the price of the product is low here. If you translate the Chinese characters as they are, you can see them as “low profits, high farms.”

In terms of economic principles, if the sale exceeds a certain amount, the unit cost will decrease and the margin will rise. In other words, sales costs should be reduced, and sales costs can be reduced through joint logistics or menu specialization.

What stores that practice delamination have in common is to reduce the number of side dishes or reduce costs through marketing strategies such as self-service and take-out. In this regard, the sale has the advantage of being able to easily manage the store anywhere with a small capital.

It also means that the sale of delamination increases the rotation, and the logic is that it absorbs more customers than before by lowering the price. However, not all stores are successful in selling off. Only stores with an appropriate size or larger can increase the turnover rate, and this also requires an appropriate rent level to enjoy the effect of delamination.

| Year | Toy Store A | A’s PV | Toy Store B | B’s PV |

| £ | £ | |||

| 0 | -375000 | -425000 | ||

| 1 | 200000 | 178571.4286 | 200000 | 178571.429 |

| 2 | 110000 | 87691.32653 | 150000 | 119579.082 |

| 3 | 220000 | 156591.6545 | 300000 | 213534.074 |

| 4 | 130000 | 82617.35019 | 250000 | 158879.52 |

| NPV | 130471.76 | 245564.1 | ||

| Payback | 2.3YEAR | 2.4YEAR |

Net Present Value (NPV) is the difference between the present value of future cash flowing from the investment and the cost invested for the investment.

Net present value (NPV) calculates the difference between the present value of the future net cash flow of the investment and the investment cost.

The higher the net present value NPV, the better, but it is difficult to be sure of the reliability of the calculation.

The level of trust in NPV results should also be considered by evaluating the rationality of the assumptions for calculation.

The Recovery Period Act is a method of evaluating an investment plan by comparing the period it takes to recover all the funds spent on the investment from the cash flow generated by the investment with the recovery period set in advance by the financial manager.

The Recovery Period Act has the advantage of reducing uncertainty about future cash flows and improving corporate liquidity, but ignoring cash flows after the recovery period makes it impossible to accurately make investments profitable and ignores the time value of money.

As a result of the analysis, A is positive for both NPV and Payback.

References

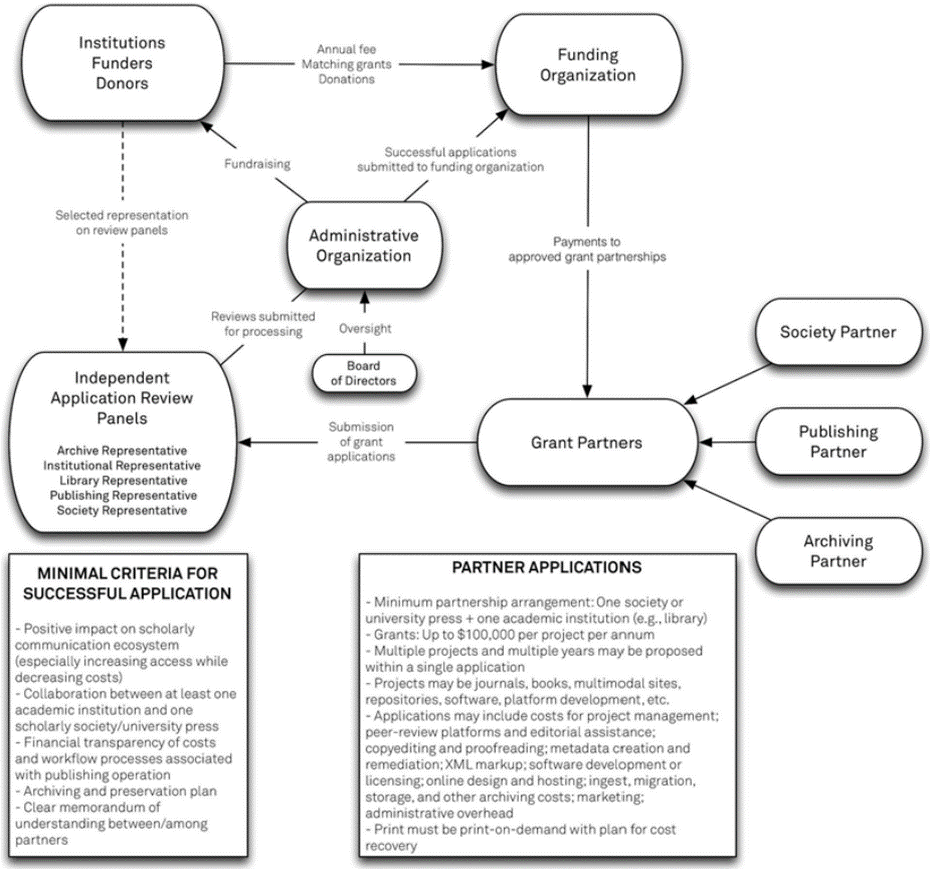

Figure 4 – available via license: Creative Commons Attribution 4.0 International (2015). [online] Available at: https://www.researchgate.net/figure/Flowchart-of-Application-Evaluation-and-Funding-Process_fig3_276655330 [Accessed 07 Mar 2015].

Use stakeholder analysis to meet the needs of all interested parties (2006). Addition. [online] Available at: https://www.techrepublic.com/article/use-stakeholder-analysis-to-meet-the-needs-of-all-interested-parties/ [Accessed 30 May 2006].

10 Types of Business Budgets to Keep Track of Your Company’s Cash (2021). Addition. [online] Available at: https://www.patriotsoftware.com/blog/accounting/types-of-business-budgets/ [Accessed 04 FEB 2021].